Overall, deferred assets play an important role in revenue recognition and business expenses. Companies must carefully track these assets to ensure that their financial statements accurately reflect their financial performance. In an installment sale, the sale price is recognized as revenue in future periods when the payments are received. The payments received are recognized as deferred assets until the sale price is fully recognized as revenue. Examples include subscriptions, maintenance contracts, and gift cards. This revenue is recorded as a liability on the balance sheet and is gradually recognized as revenue over the period in which the goods or services are provided.

It’s important for companies to keep track of all liabilities, even the short-term ones, so they can accurately determine how to pay them back. On a balance sheet, these two categories are listed separately but added together under “total liabilities” at the bottom. The portion of the vehicle that you’ve already paid for is an asset. Financial liabilities can be either long-term or short-term depending on whether you’ll be paying them off within a year. A contingent liability is an obligation that might have to be paid in the future but there are still unresolved matters that make it only a possibility, not a certainty.

A deferred asset is an asset that will be realized in the future, while a prepaid expense is a payment made for goods or services that will be received in the future. This ensures that what are examples of liabilities the company’s financial statements accurately reflect the true cost of the asset and the revenue it generates. In conclusion, deferred assets are an important part of financial accounting. Companies must account for deferred assets properly to ensure that their financial statements are accurate and comply with accounting rules. By following GAAP or IFRS, companies can provide investors and other stakeholders with transparent and reliable financial statements.

You can prioritize which debts to pay off first based on their terms and rates. Understanding them can empower you to take control of your financial future and avoid potential pitfalls along the way. It means being responsible for compensating someone for any harm or damage you cause. This could happen due to negligence, breaking a contract, or any other wrongful actions.

On a balance sheet, liabilities show a company’s financial obligations to its lenders and creditors due to past transactions. They occur on the right side of the balance sheet and are divided into current and long-term liabilities. These liabilities provide an overall view of a company’s financial commitments. For example, when a company borrows money from a bank, it creates a financial liability. In another case, if a business buys products on credit, it creates a liability to pay the supplier later. Knowing about these various types of liabilities is very important for people and businesses to manage their money well.

Deferred assets are a common accounting concept that can be difficult to understand for those who are new to the field. Essentially, a deferred asset is an item that has been paid for but has not yet been used or consumed. This can include a variety of different things, such as prepaid expenses, unearned revenue, and deferred tax assets. Liabilities are a broader category that includes both agreed and not agreed obligations. Companies calculate deferred tax assets based on the difference between their financial statements and tax returns. Deferred tax assets are created when a company has overpaid taxes or has tax credits or deductions that will be realized in the future.

When a company depreciates an asset for accounting purposes, it reduces its accounting income, but this does not necessarily reduce its taxable income. As a result, the company may be required to create a deferred tax asset to represent the tax benefit that will be realized in future years as a result of the depreciation. In a 401(k) plan, the contributions made by an employee are deferred assets until the employee retires and starts receiving the benefits. The contributions are recognized as expenses in the current period but will be recognized as revenue in future periods when the employee starts receiving the benefits.

In most cases, lenders and investors will use this ratio to compare your company to another company. A lower debt to capital ratio usually means that a company is a safer investment, whereas a higher ratio means it’s a riskier bet. Another popular calculation that potential investors or lenders might perform while figuring out the health of your business is the debt to capital ratio. Current liabilities are debts that you have to pay back within the next 12 months. A liability is anything you owe to another individual or an entity such as a lender or tax authority.

On the other hand, an example of a deferred obligation is an overpayment. When a customer overpays an invoice, the amount is recognized as a deferred obligation until the company can return the overpayment. Once the overpayment is returned, the deferred obligation is no longer recorded on the balance sheet.

This results in a temporary difference, with the tax basis being lower than the reported amount in the financial statements. Overall, deferred assets are an important aspect of financial reporting and can have a significant impact on a company’s cash flow. Companies should carefully consider the accounting treatment of deferred assets and ensure that they are properly recorded and recognized in their financial statements.

The revenue is recorded as a deferred asset on the balance sheet until the warranty period is complete. Timing differences occur when there is a difference between the timing of when an item is recognized for tax purposes and when it is recognized for financial reporting purposes. This can result in temporary differences, which are the differences between the tax basis of an asset or liability and its reported amount in the financial statements. For example, if a company receives payment for a service that will be provided over the course of a year, it would record the payment as deferred revenue. As the service is provided, the company would recognize the revenue earned each month until the full amount of the payment has been earned.

Read on to learn more about the importance of liabilities, the different types, and their placement on your balance sheet. Companies of all sizes finance part of their ongoing long-term operations by issuing bonds that are essentially loans from each party that purchases the bonds. This line item is in constant flux as bonds are issued, mature, or called back by the issuer. Liabilities are categorized as current or non-current depending on their temporality.

These assets are recorded on the balance sheet as an asset and are expected to provide future economic benefits to the company. Deferred assets can be a useful tool for companies to manage their cash flow and financial obligations. However, they must be carefully monitored to ensure they are properly accounted for and do not distort the company’s financial position.

A company must therefore consider how it will finance its non-current liabilities in the long term. This means that it has to pay a debt to another company or a private person. A classic example is a bank loan that must be repaid to the bank in monthly instalments. Contingent liabilities are types of liabilities that may or may not occur depending on the outcome of a future event. If they are found to be guilty, they would have to pay for damages. In contrast, the table below lists examples of non-current liabilities on the balance sheet.

These include the ownership of tangible assets, financial resources, and accounts receivable and inventory. They are thus the counterpart to liabilities, which include debts, mortgages, tax payments and account payables. Liabilities in accounting are recorded as financial obligations, but these act as the most efficient resource for companies to fund capital expansion.

Liabilities are reported on a company’s balance sheet and determine its financial health. Liabilities are an operational standard in financial accounting, as most businesses operate with some level of debt. Unlike assets, which you own, and expenses, which generate revenue, liabilities are anything your business owes that has not yet been paid in cash. The most common liabilities are usually the largest such as accounts payable and bonds payable. Most companies will have these two-line items on their balance sheets because they’re part of ongoing current and long-term operations. Deferred tax assets can also arise from other temporary differences between accounting income and taxable income, such as depreciation.

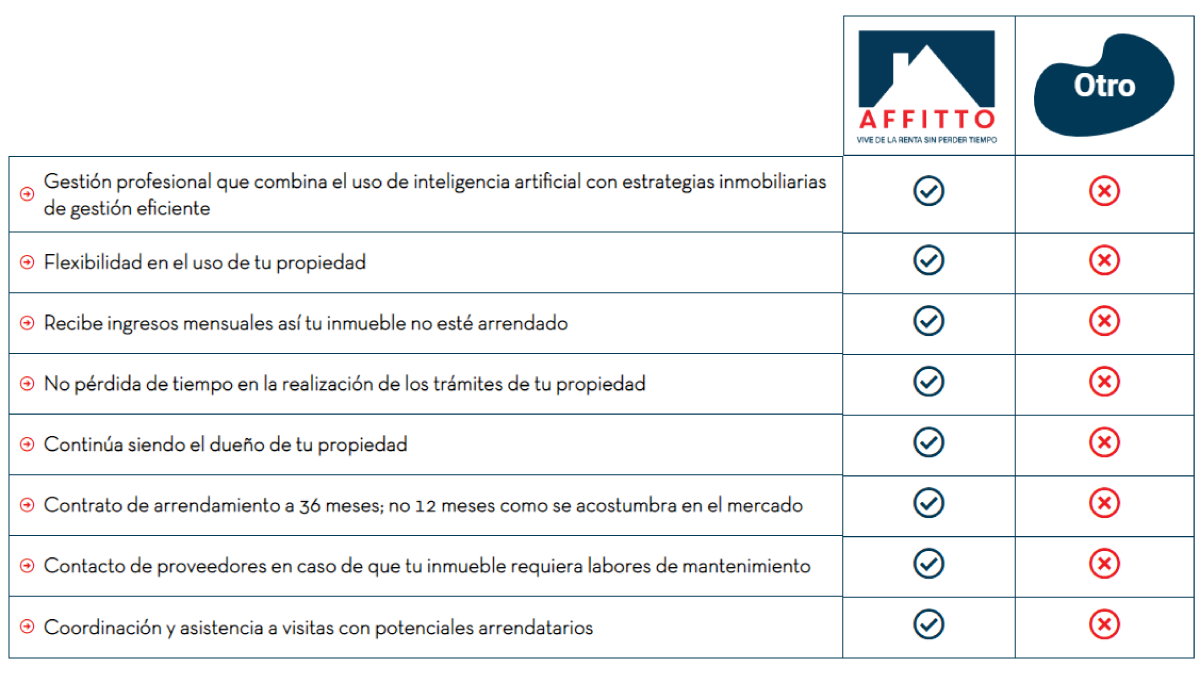

Permanencia: Por un periodo de 36 meses

Cuando aportas tu propiedad a Affitto te comprometes a que tu inmueble esté gestionado por nosotros por un periodo de 36 meses, podrás retirarte cumpliendo los periodos de notificación anticipada y cumpliendo con la penalización por terminación anticipada del contrato

Tareas que realiza Affitto

Nos encargamos de toda la gestión comercial y operativa de tu propiedad por medio de un equipo profesional que se apoya en tecnología avanzada: a.) Definición de la estrategia óptima de comercialización, incluyendo la definición del mejor canon de arrendamiento a cobrar, así como registros fotográficos, publicación en canales digital y físicos, muestra el inmueble a potenciales arrendatarios b.) Gestión operativa de tu propiedad, lo que incluye: 1.Relacionamiento con el propietario 2.Coordinación de mantenimientos y reparaciones 3.Cobro del canon de arrendamiento

Comisión de Affitto

Por la realización de nuestras labores (incluyendo comercialización y garantía del canon de arrendamiento mientras se encuentre vacante) cobramos una comisión del 20% sobre los ingresos brutos mensuales cuando el inmueble se encuentre arrendado.