Eg both women and men old 18 to help you 64, their alternatives aged 65 and over was in fact plus more susceptible in order to being in the lowest-money situation after they weren’t part of one or two (Chart 8). During the 2015, 33.0% from unattached older female were inside the low income, since was in fact 30.8% of their male alternatives. In contrast, 8.7% regarding the elderly in the partners was indeed inside the lower income.

On lack of money gotten by way of regulators transfers, twenty-seven.1% out of girls and female will have stayed in lowest-money properties inside the 2015, as opposed to the fourteen.7% of girls and you can women who actually did very (Chart 9). To phrase it differently, the brand new proportion from girls and you will women in low income could have been 12.cuatro fee affairs large had been it perhaps not into the regulators tax and you will transfer program. This program got the same effect on boys and you will men, decreasing the proportion ones living in lowest-income families by the 10.step three percentage factors, out-of 24.0% to help you thirteen.7%.

The newest share out of bodies transmits so you can reducing money inequality is most apparent one particular aged 65 as well as over, for example senior women: 52.3% of those female might have been from inside the low income inside the 2015, instead of the 16.3% of these who in reality performed, had been they not to possess bodies transfers (a positive change away from thirty six.0 fee points). Also, new ratio from reduced-earnings senior guys could have been 32.1 percentage affairs highest white man Hue women was indeed they perhaps not getting regulators transfers (forty-two.0% instead of eleven.9%).

Money and you will wide range is relevant- however, line of- rules. Income is the «flow» of cash generated more certain time, if you find yourself money refers to the property value property, particularly an owned family, old age coupons, carries and you will securities, motor vehicles, and you can local rental features, less the worth of debts (or obligations). Notice 46 Money may either be used having expose practices otherwise transformed into wealth as a result of saving otherwise purchasing. Property accumulated previously can also be next be marketed, plus in that way transformed into introduce practices. Hence, money also have financial security inside issues out-of financial hardship, such as business loss, disability, or dying.

For many Canadians, the most valuable house is the family; through the years, wide range or «equity» adds up due to the fact mortgage for the house is slowly paid additionally the market price of the property values. Past home ownership, construction conditions- affordability, adequacy, and viability- reflect financial really-getting. Casing is recognized as being sensible when children spends reduced than simply 31% of its pre-taxation earnings on it; sufficient whether or not it doesn’t have major fixes; and you may appropriate in the event it provides a sufficient number of rooms to have the size and constitution of the family (we.age. , perhaps not congested).

The possibilities of owning a home relies on many years, sex, and you may loved ones sort of. A lot of the people in couples lived-in a home owned (rather than rented) by on your own or children affiliate: 79.8% of these old 18 in order to 64 and you can 88.9% of those old 65 as well as performed so in the 2015 (Desk 1). Significant gender variations in the likelihood of home ownership should be observed one of solitary moms and dads: 38.2% out of lone moms and dads lived-in a home belonging to oneself or children representative, in contrast to 62.0% out-of solitary fathers (a difference out-of 23.8 commission products). Though unattached elderly feminine was indeed more likely than simply lone moms and dads to live-in a home owned by children representative, they were equally likely to get it done as the senior dudes (57.3% and 58.3% respectively). Unattached gents and ladies old 18 to 64 that has no children was basically in addition to likewise going to live-in an owned home: forty.2% and 38.4%, respectively. Notice 47

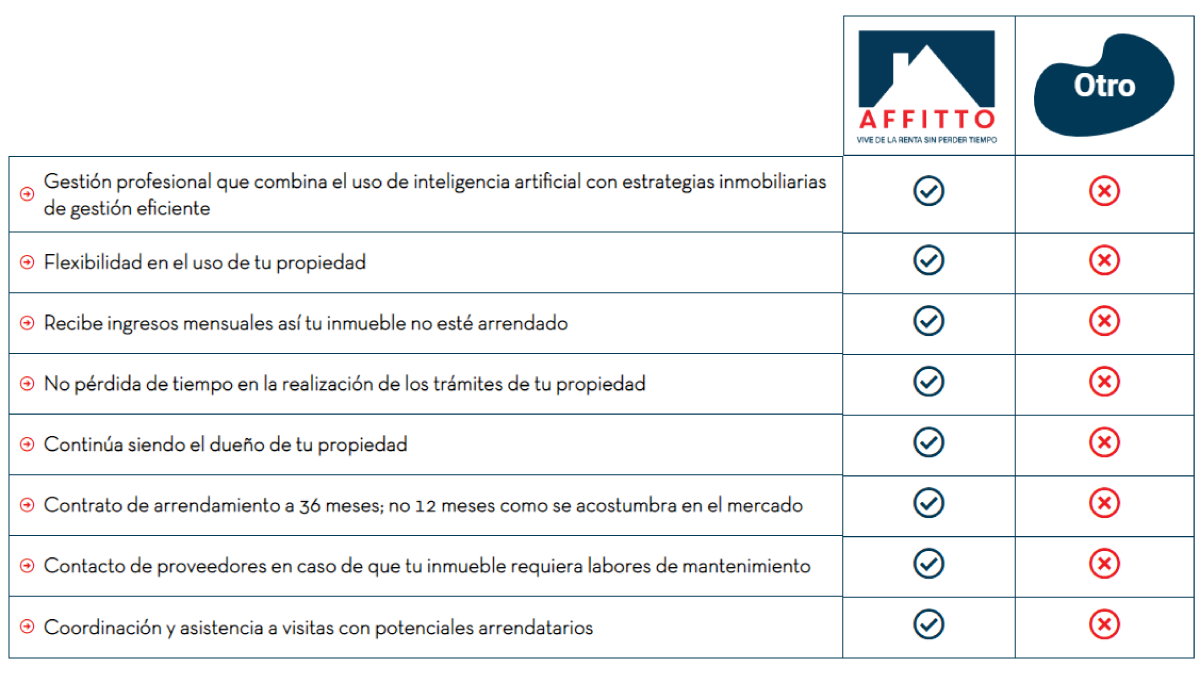

Permanencia: Por un periodo de 36 meses

Cuando aportas tu propiedad a Affitto te comprometes a que tu inmueble esté gestionado por nosotros por un periodo de 36 meses, podrás retirarte cumpliendo los periodos de notificación anticipada y cumpliendo con la penalización por terminación anticipada del contrato

Tareas que realiza Affitto

Nos encargamos de toda la gestión comercial y operativa de tu propiedad por medio de un equipo profesional que se apoya en tecnología avanzada: a.) Definición de la estrategia óptima de comercialización, incluyendo la definición del mejor canon de arrendamiento a cobrar, así como registros fotográficos, publicación en canales digital y físicos, muestra el inmueble a potenciales arrendatarios b.) Gestión operativa de tu propiedad, lo que incluye: 1.Relacionamiento con el propietario 2.Coordinación de mantenimientos y reparaciones 3.Cobro del canon de arrendamiento

Comisión de Affitto

Por la realización de nuestras labores (incluyendo comercialización y garantía del canon de arrendamiento mientras se encuentre vacante) cobramos una comisión del 20% sobre los ingresos brutos mensuales cuando el inmueble se encuentre arrendado.