Its current liabilities, meanwhile, consist of $100,000 in accounts payable. In this scenario, the company would have a current ratio of 1.5, calculated by dividing its current assets ($150,000) by its current liabilities ($100,000). The current ratio is balance-sheet financial performance measure of company liquidity. The current ratio indicates a company’s ability to meet short-term debt obligations. The current ratio measures whether or not a firm has enough resources to pay its debts over the next 12 months.

In this guide, we’ll provide an overview of the cash ratio definition and formula, and the important insights that this metric provides to business leaders. In certain cases, businesses need to know what they’re able to cover using the cash that’s already available, which the aptly-named cash ratio helps measure. When a company is figuring out how to meet its short-term liabilities, expected future cash flows might not make a big difference in their decision-making. A cash ratio between 0.5 and 1.0 is generally healthy for most large, mature tech companies. These firms often generate steady cash flows and don’t need to hold excessive cash.

This is because inventory can be more challenging to convert into cash quickly than other current assets and may be subject to write-downs or obsolescence. Inventory management issues can also lead to a decrease in the current ratio. If the company holds what is the purpose of preparing an income summary and an income statement chron com too much inventory that is not selling, it can tie up cash and reduce the current ratio. For example, a manufacturing company that produces goods may have a lower current ratio than a service-based company that does not have to maintain inventory. Creditors and lenders often use the current ratio to assess a company’s creditworthiness.

It tells you how much investors are paying for each dollar of actual operating cash flow. Both variables are shown on the balance sheet (statement of financial position). Instead, we should closely observe this ratio over some time – whether the ratio is showing a steady increase or a decrease. Instead, there is a clear pattern of seasonality in current ratio equations.

An excessively high CR , above 3, could mean that the company can pay its short-term debts three times. Like the quick ratio, the rationale behind this approach is that inventory and A/R may be difficult to convert to cash and thus may inflate a company’s perceived ability to meet short-term obligations. A criticism of the cash ratio is that it may be too conservative and underestimate a company’s ability to sell through inventory and to collect on its A/R. Companies can explore ways they can re-amortize existing term loans and change the interest charges from lenders.

Nevertheless, a company with a very high current ratio, say 3.0 compared to its peer group may not necessarily mean that the company can cover its current liabilities three times. It could mean that the management may not be using the company’s current assets or its short-term financing facilities efficiently. It could be an indication that the company’s working capital is not properly managed and is not securing financing very well. Investors can use this type of liquidity ratio to make comparisons with a company’s peers and competitors. Ultimately, the current ratio helps investors understand a company’s ability to cover its short-term debts with its current assets. It indicates the financial health of a company and how it can maximize the liquidity of its current assets to settle debt and payables.

These current assets include items such as accounts receivable, cash, inventory, and other current assets (OCA) that are expected to be liquidated or turned into cash within a year. The current liabilities, on the other hand, include wages, accounts payable, short-term debts, taxes payable, and the current portion of long-term debt. The current ratio calculator allows you to calculate your current ratio, which is a sign of the short-term financial health of your company. It determines whether a company’s current assets are sufficient to cover its current liabilities. The current ratio divides a company’s current assets by its current liabilities.

Company B has more cash, which is the most liquid asset, and more accounts receivable, which could be collected more quickly than liquidating inventory. Although the total value of current assets matches, Company B is in a more liquid, solvent position. Current assets listed on a company’s balance sheet include cash, accounts receivable, inventory, and other current assets (OCA) that are expected to be liquidated or turned into cash in less than one year. Depending on whether the present ratio is within or above the desired range, the appropriate approach may vary. Businesses may use these methods to improve accounts receivable collections, sell fixed assets, save expenses, manage accounts payable, and invest assets, among other things. Any balance sheet item, including liquid assets, that may be converted to cash within a year is considered a current asset.

Many SMBs maintain a 30% to 50% debt mix, leveraging borrowed funds to support growth while relying on equity for stability. Striking the right balance is key to managing financial risk and sustainable growth. The cash ratio is just one metric businesses can use to evaluate their financial health and drive strategic decisions. Thus, it’s typically not difference between shareholder and stockholder helpful to perform a ratio analysis of a company and compare its cash ratio against businesses in other industries. The cash ratio has been criticized for being overly cautious, underestimating a company’s capacity to sell goods and collect accounts receivable. If the business is holding a surplus of assets, it’s missing out on opportunities to reinvest that capital into their business.

Other measures of liquidity and solvency that are similar to the current ratio might be more useful, depending on the situation. For instance, while the current ratio takes into account all of a company’s current assets and liabilities, it doesn’t account for customer and supplier credit terms, or operating cash flows. On the other hand, the quick ratio is calculated by subtracting inventory from current assets and dividing the result by current liabilities. The quick ratio is considered a more conservative measure of a company’s ability to meet its short-term obligations. A current ratio of 1.5 would indicate that the company has $1.50 of current assets for every $1 of current liabilities. For example, suppose a company’s current assets consist of $50,000 in cash plus $100,000 in accounts receivable.

While all three ratios have some overlap in their formulas and input values, they each offer a distinct measure of liquidity. As such, they’re often used side by side to help teams get a more comprehensive picture of the business’s liquidity. A cash ratio above 1.0 means the company has more cash than it needs to meet its obligations. It could pay off all debts due for the year, and still have some cash left over. A ratio below 1.0 means that its short-term debts outsize the cash on hand, which could point to potential insolvency.

This is why it is helpful to compare a company’s current ratio to those of similarly-sized businesses within the same industry. The cash flow coverage ratio determines the credit risk of a company or business by comparing its OCF (Operating Cash Flow) and total outstanding debt. It signifies the business’s ability to meet debt obligations using its operating cash flow. The current ratio is a helpful measure for assessing a company’s short-term financial health by determining its capacity to pay current obligations with current assets. However, although it is a basic and useful model for many organizations, it may fall short of properly assessing the financial health of enterprises with certain kinds of assets or in specific sectors.

To calculate the ratio, analysts compare a company’s current chart of accounts assets to its current liabilities. A ratio under 1.00 indicates that the company’s debts due in a year or less are greater than its cash or other short-term assets expected to be converted to cash within a year or less. The cash ratio isn’t the only liquidity ratio stakeholders can use to evaluate a company’s ability to meet near-term obligations.

Many entities have varying trading activities throughout the year due to the nature of industry they belong. The current ratio of such entities significantly alters as the volume and frequency of their trade move up and down. In short, these entities exhibit different current ratio number in different parts of the year which puts both usability and reliability of the ratio in question.

However, the end result of the calculation could mean different things based on the result. Let us understand how to interpret the data from a current ration calculator through the discussion below. It’s important to set goals for the current ratio, but it should come from an equal consideration of industry norms and the unique aspects of the business. The rule of thumb is that a “good” current ratio is greater than 1.0 and that 1.5 to 2.0 is the target to aim for.

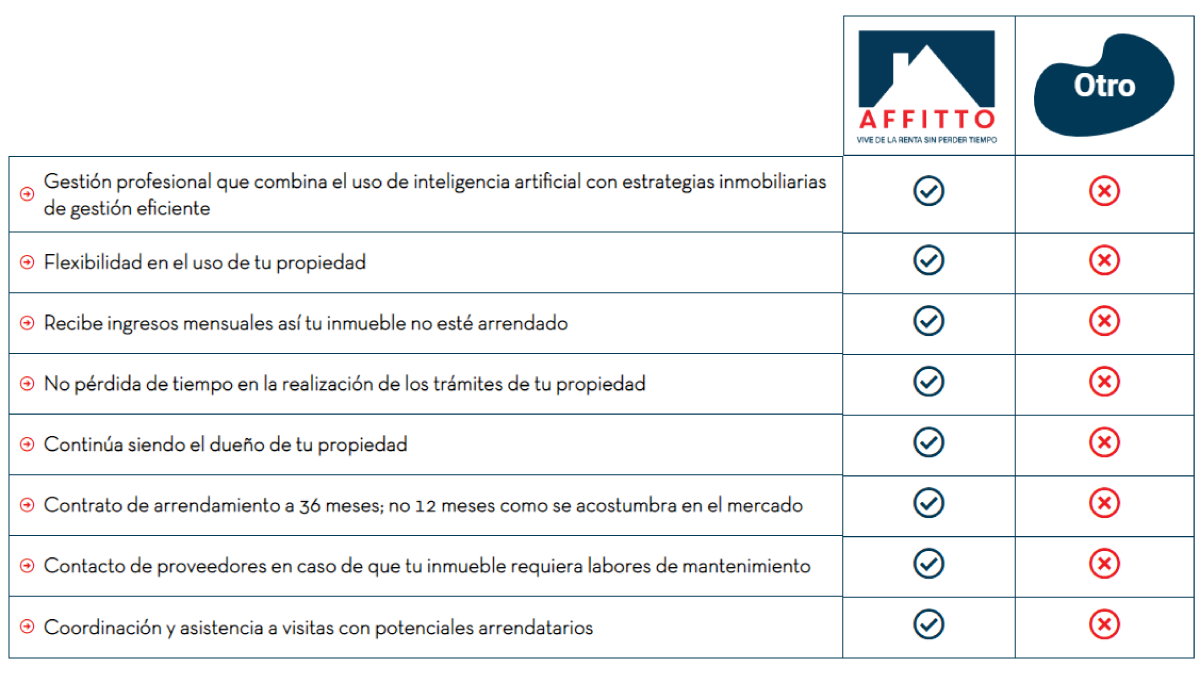

Permanencia: Por un periodo de 36 meses

Cuando aportas tu propiedad a Affitto te comprometes a que tu inmueble esté gestionado por nosotros por un periodo de 36 meses, podrás retirarte cumpliendo los periodos de notificación anticipada y cumpliendo con la penalización por terminación anticipada del contrato

Tareas que realiza Affitto

Nos encargamos de toda la gestión comercial y operativa de tu propiedad por medio de un equipo profesional que se apoya en tecnología avanzada: a.) Definición de la estrategia óptima de comercialización, incluyendo la definición del mejor canon de arrendamiento a cobrar, así como registros fotográficos, publicación en canales digital y físicos, muestra el inmueble a potenciales arrendatarios b.) Gestión operativa de tu propiedad, lo que incluye: 1.Relacionamiento con el propietario 2.Coordinación de mantenimientos y reparaciones 3.Cobro del canon de arrendamiento

Comisión de Affitto

Por la realización de nuestras labores (incluyendo comercialización y garantía del canon de arrendamiento mientras se encuentre vacante) cobramos una comisión del 20% sobre los ingresos brutos mensuales cuando el inmueble se encuentre arrendado.